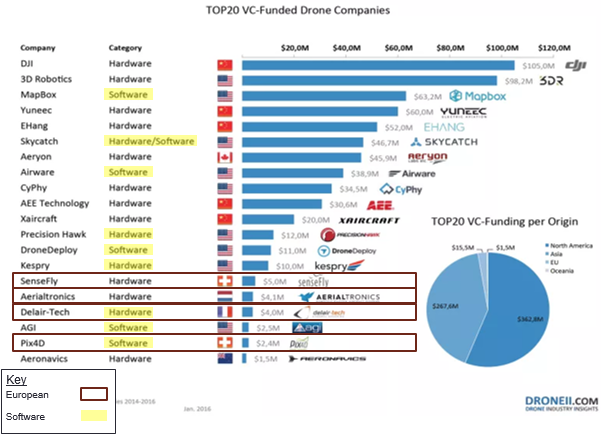

Let’s talk a little about what some of these companies actually do.

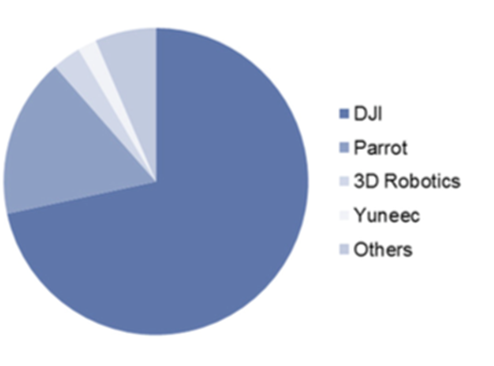

DJI: By far the biggest drone platform manufacturer, dominant when it comes to both consumer and commercial drones (more on this later). Interestingly, DJI and investor Accel have teamed up to start the SkyFund, an investment fund for drone startups.

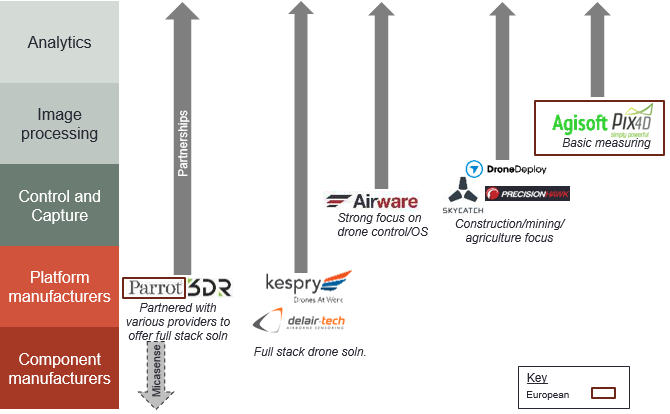

3D Robotics: Another platform manufacturer. Anecdotally, they’re pivoting to be more commercially focused in light of DJI’s dominance in consumer drones. They’re also trying to get more involved in the software stack, and have forged partnerships with the likes of Autodesk to allow commercial users to do mapping and analysis.

Yuneec: Also a platform manufacturer — both consumer and commercial drones. The Typhoon series is quite a highly rated consumer drone and at $1,300 is said to be a commercial level drone at consumer price. I’ve not used a Yuneec drone, but they’re meant to have quite advanced sense and avoid technology with Intel’s Realsense technology

Mapbox: It’s not really fair to put this down as a “drone” startup, as Mapbox is all about custom maps, with data taken from both open data sources such as OpenStreetMap and NASA, and from proprietary data sources such as DigitalGlobe. However, you can also feed in aerial data from drones and generate maps — but this is not the primary use case.

Skycatch: Their drone platform hasn’t yet been released, so for now they’re more of a software play. They’ve got an app which you can use to control a DJI drone and use to capture the data you need. They’ve also got an analytics dashboard to do things like overlay construction plans, annotate images, track progress etc.

Aeryon: A commercial drone platform specialist. Their drones are meant to perform well in harsh environments, extreme weather, high winds etc.

Airware: They want to be the universal OS for drones. Through some hardware plugins, you can plan flights, control a drone and make use of its various sensors / payload etc. Data collected is fed back to an aerial information platform, which can be used to carry out analytics on the data. They’ve also launched a “Commercial Drone Fund”, another fund for drone startups (which was actually launched on the same day as the DJI/Accel SkyFund).

PrecisionHawk: It’s listed above as a hardware company, but in reality it is both hardware and software. They do have their own fixed wing craft but are also very involved in the software play. They’re involved in the full software stack, with an analytics package focused on precision agriculture.

Drone Deploy: They offer a suite of software products covering the entire stack from drone control to image processing to analytics. The industries they tend to focus on are construction, mining and precision agriculture.

Kespry: Again, I’ve highlighted them as a software company because in addition to their own drone they do offer the full software stack targeting the construction industry

Sensefly: The French company Parrot has a controlling stake in Sensefly, which primarily makes fixed wing drones for commercial data collection. They do also have some involvement in sensor hardware (they have a multispectral depth camera), and the company is integrated such that Parrot can offer end-to-end solutions for particular verticals (e.g., the “Sequoia” solution for precision agriculture).

Delair Tech: They can offer both hardware (in the form of long range drones), or software for image analysis, or drones-as-a-service for commercial clients in construction, agriculture and infrastructure. Interestingly they are also able to mix satellite data for analysis

AGI: This is actually more of a satellite company than a drone company: it’s all about modelling / simulation software for satellites. For example you can model sensors and payloads, run simulations on the transmitters, receivers etc.

Pix4D: One of the most widely used 3D reconstruction / modelling software packages for aerial data. Pix4D also offers some basic analysis tools like volume estimation etc.